For clients and investors needing insights into Africa

About

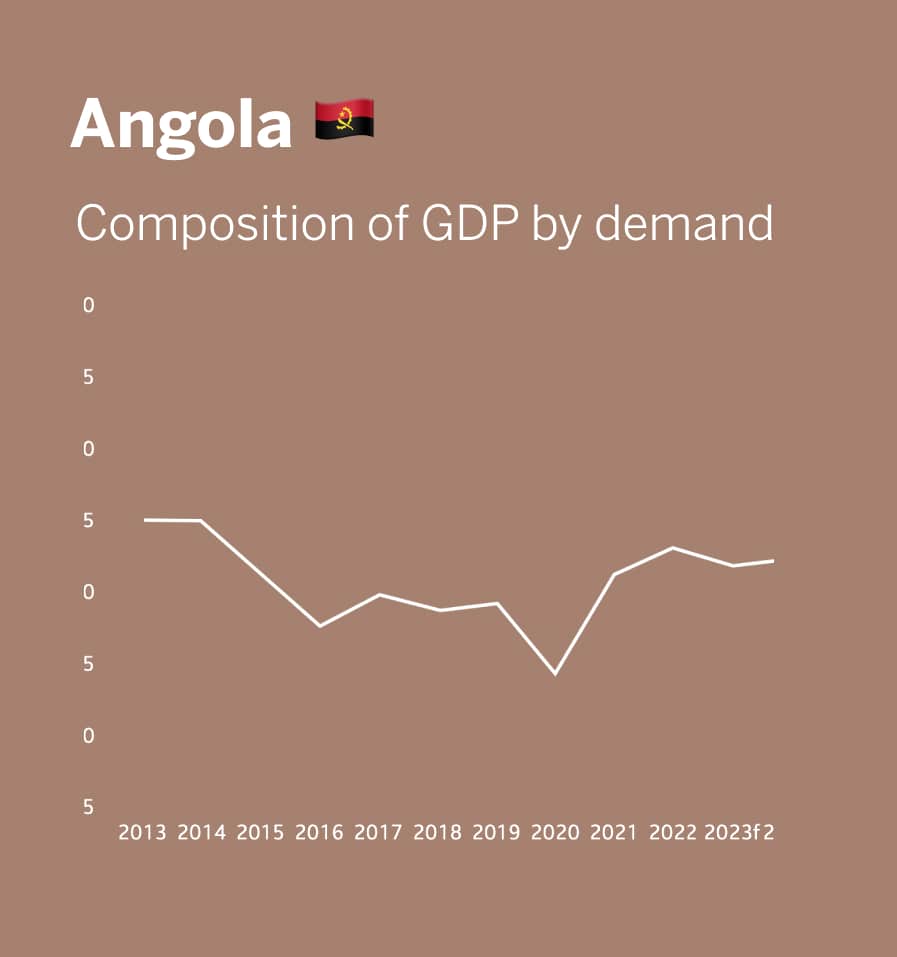

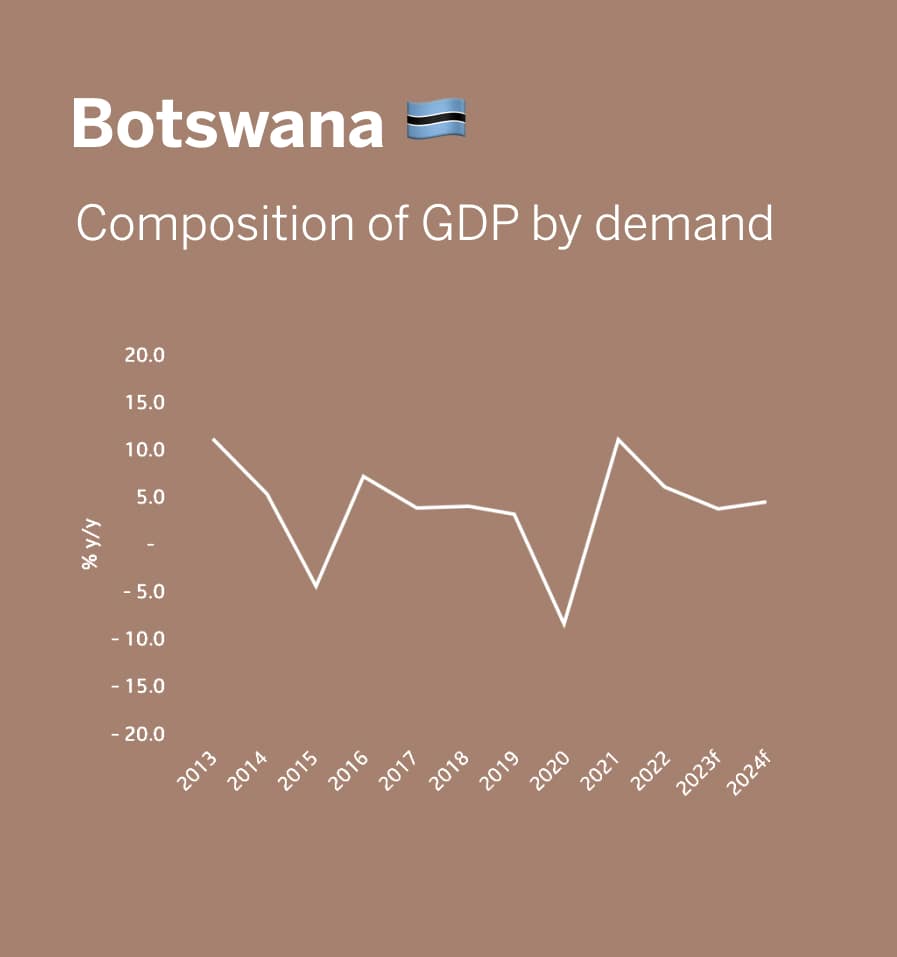

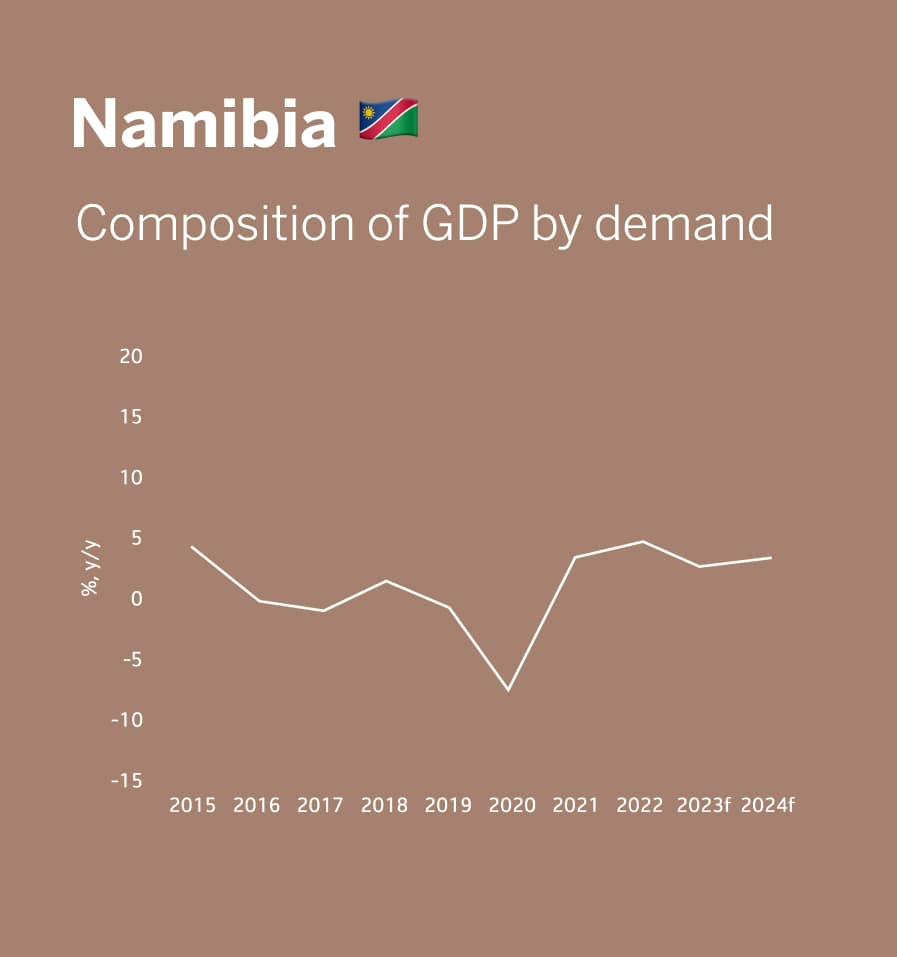

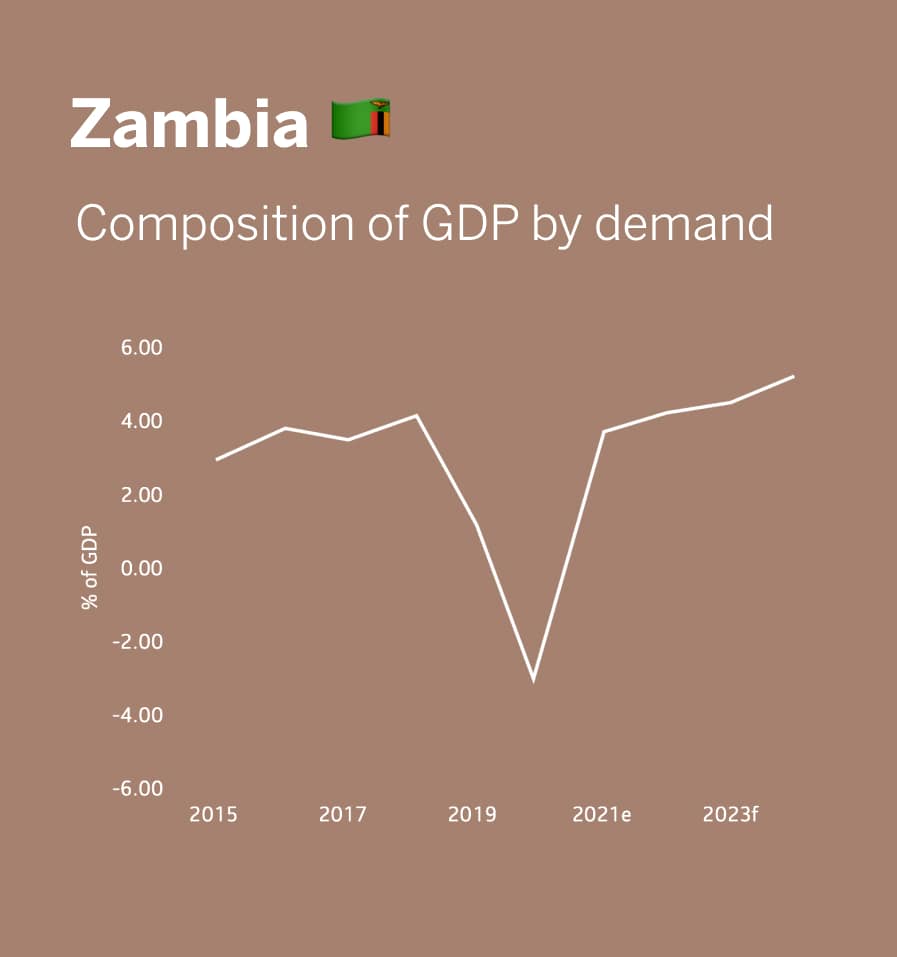

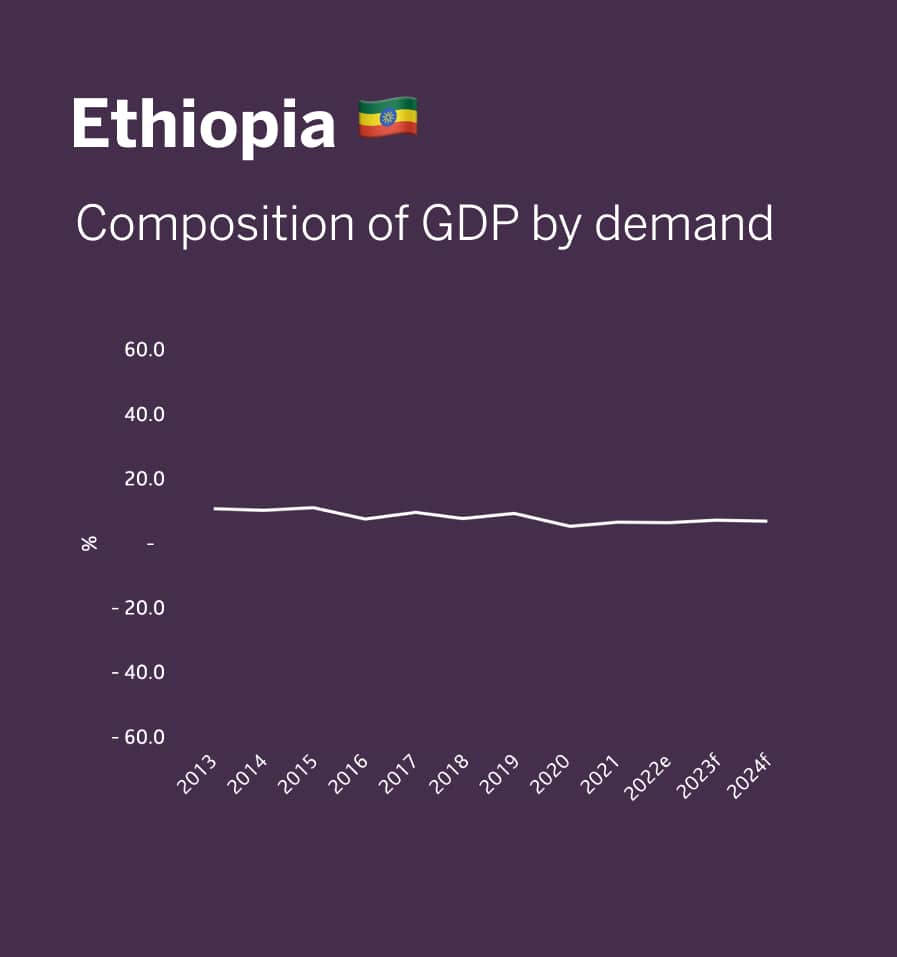

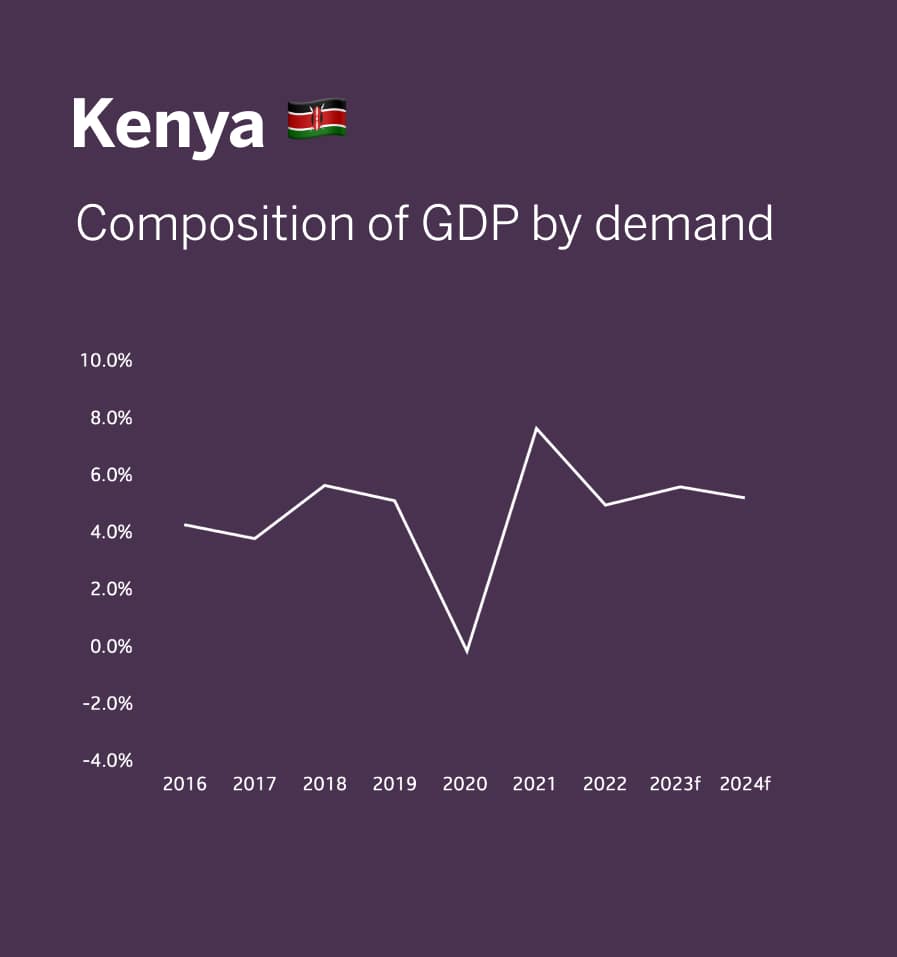

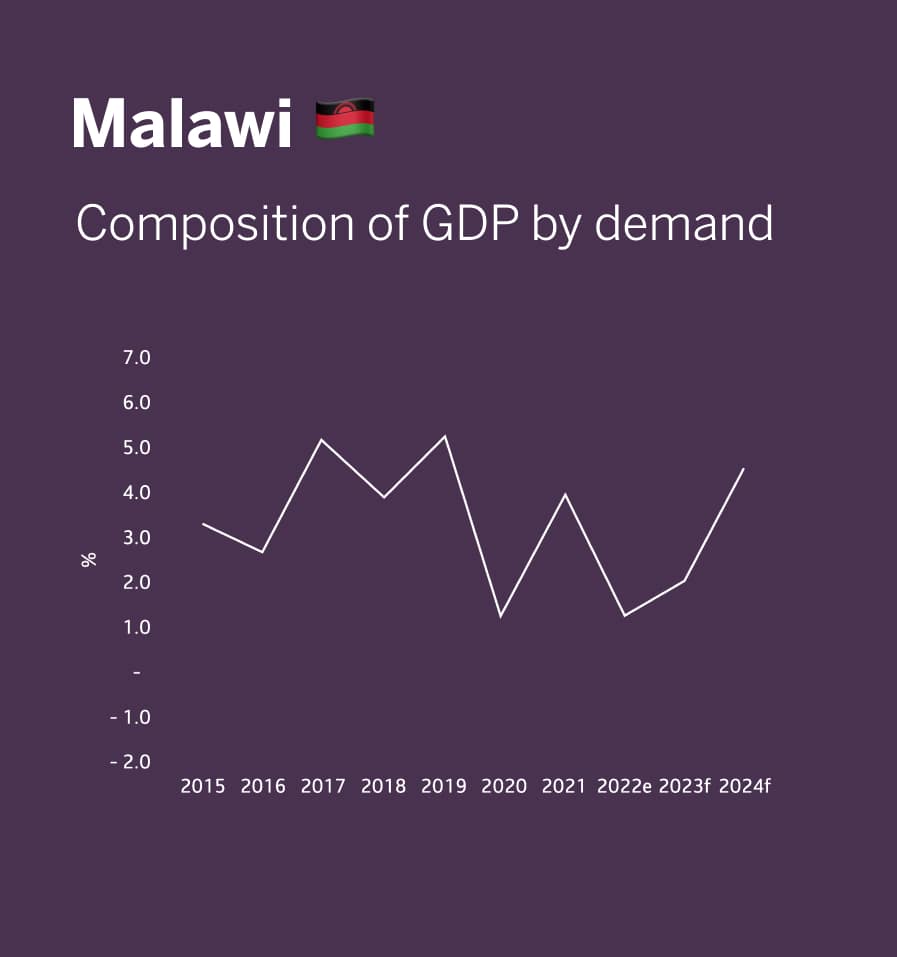

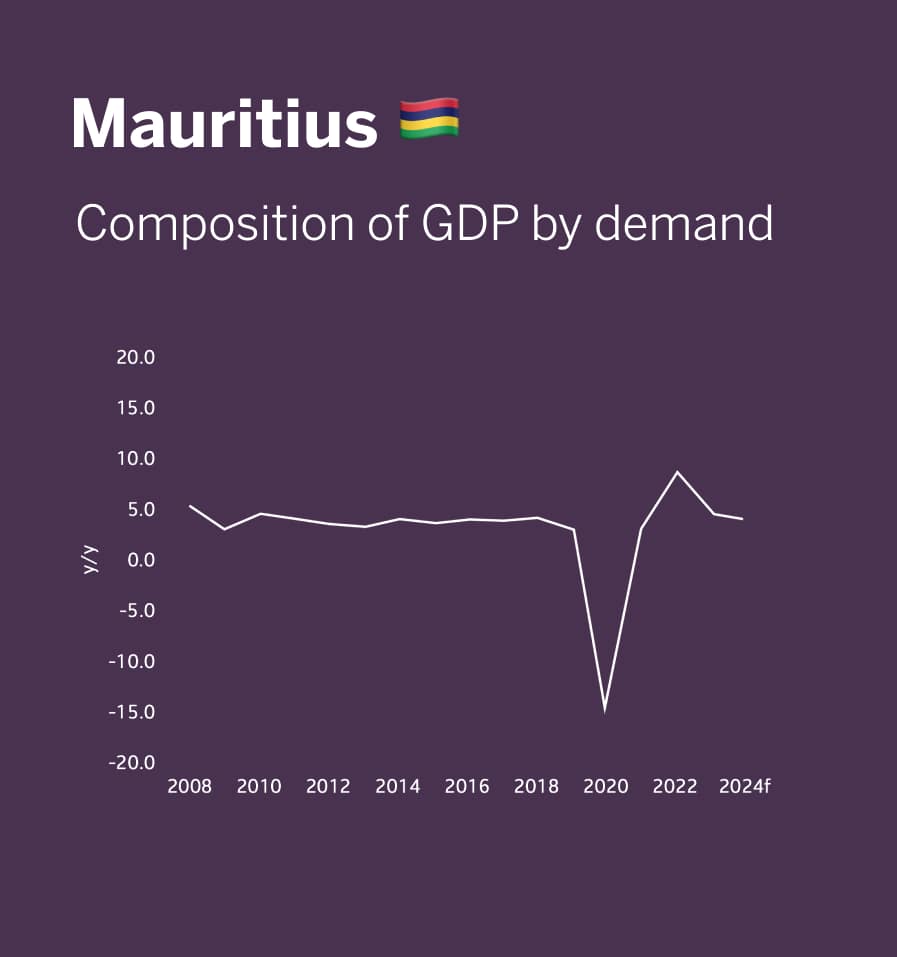

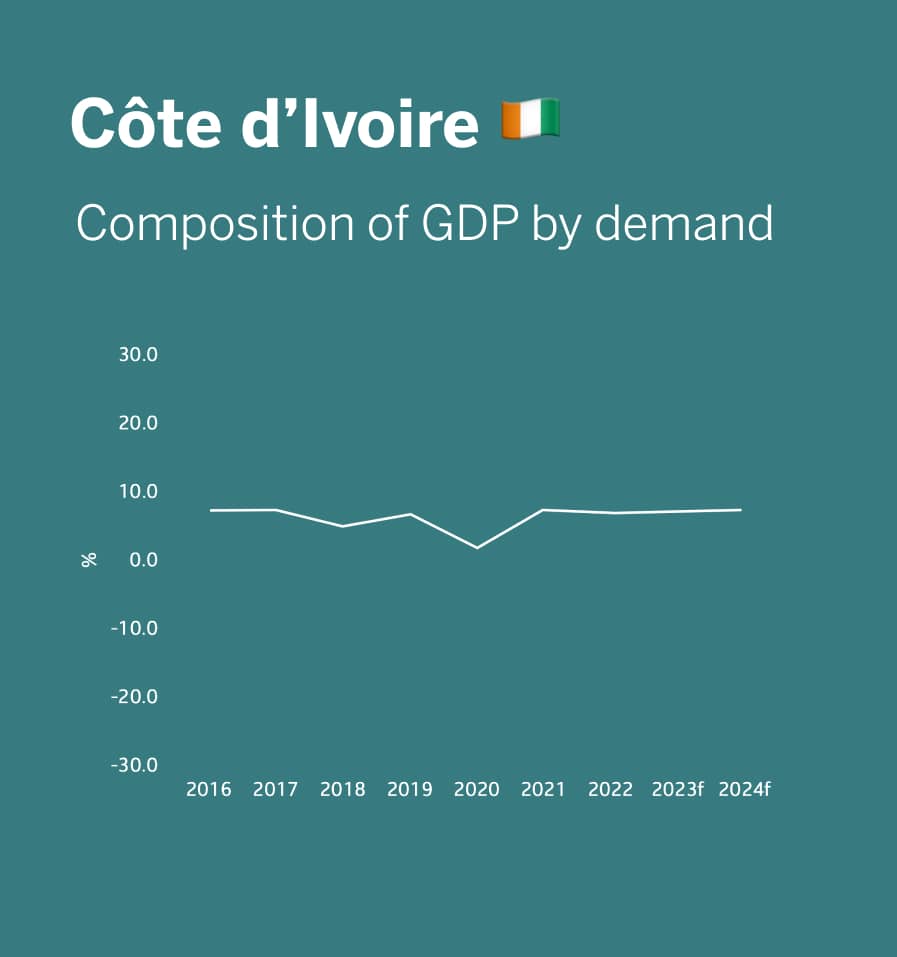

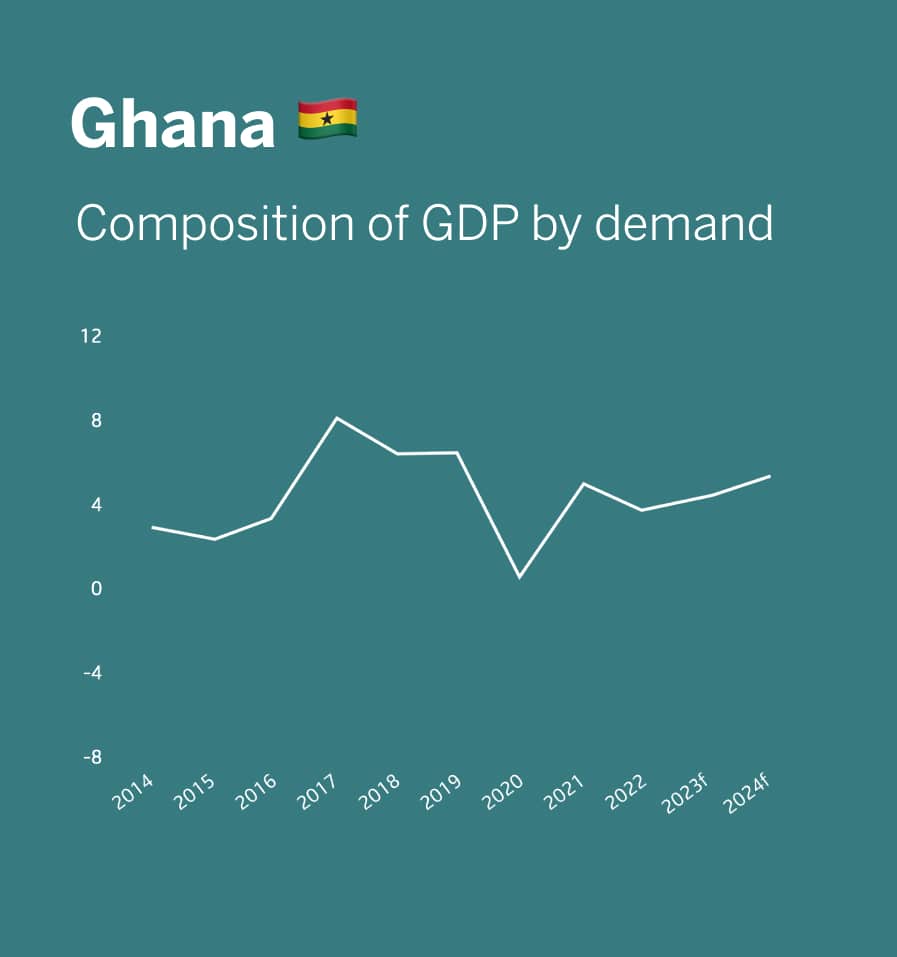

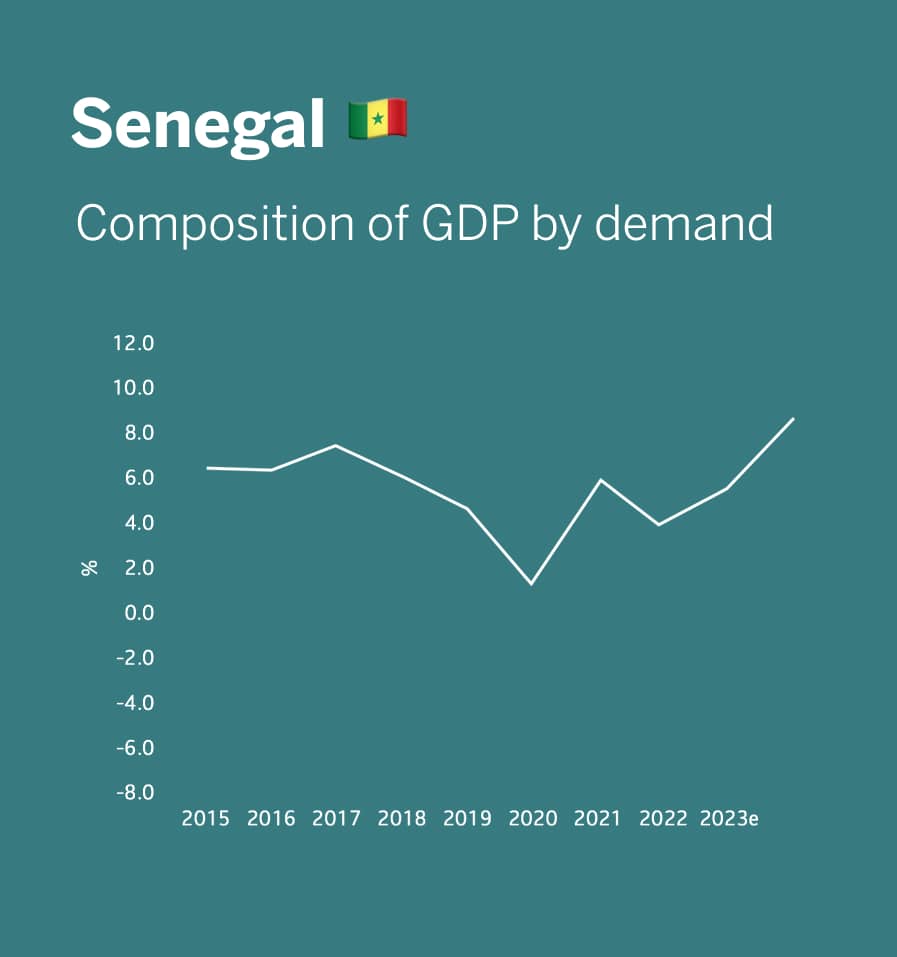

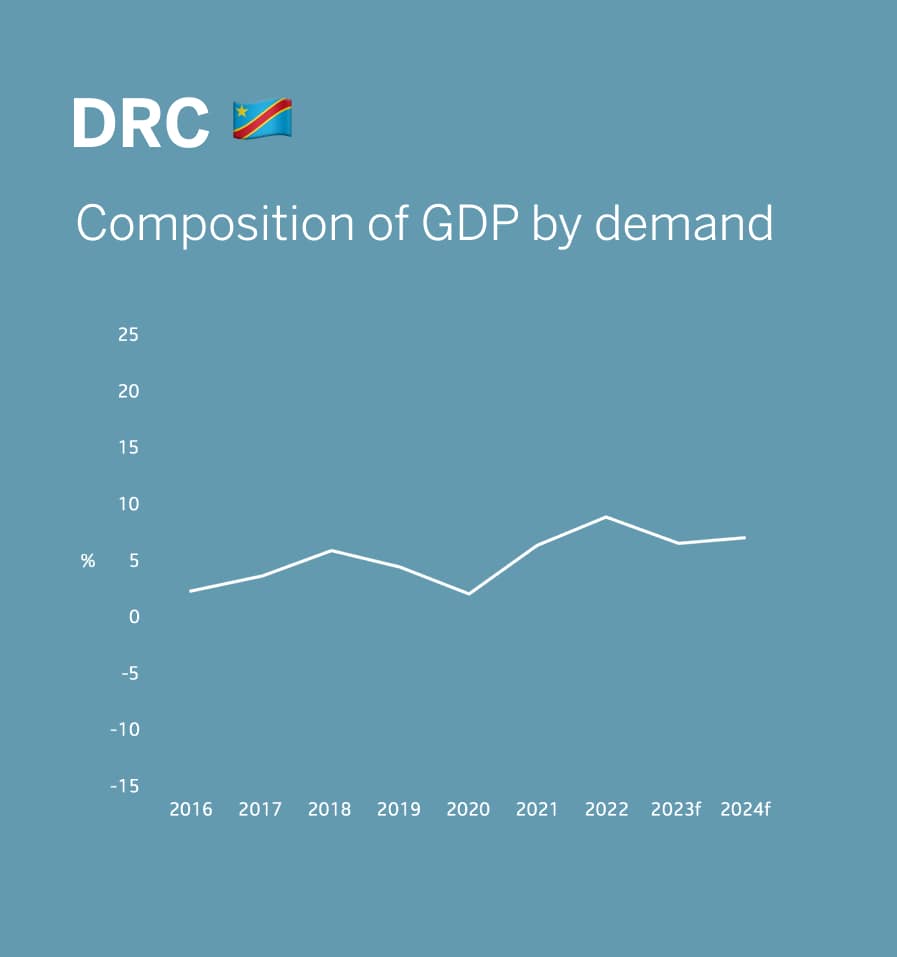

In 2023, global economic growth is anticipated to decrease compared to the previous year, despite upward revisions in growth estimates since January 2023. Notably, African economic growth is expected to remain resilient, with a significant reliance on private consumption expenditure, which typically accounts for 60% to 70% of GDP in most covered markets. This emphasizes a greater dependency on domestic demand rather than external demand. However, the forthcoming El Niño event, projected to commence in Q4:23, could potentially impact the growth outlook for the year, as it may bring excessive rainfall to East Africa and drier conditions to parts of southern Africa.

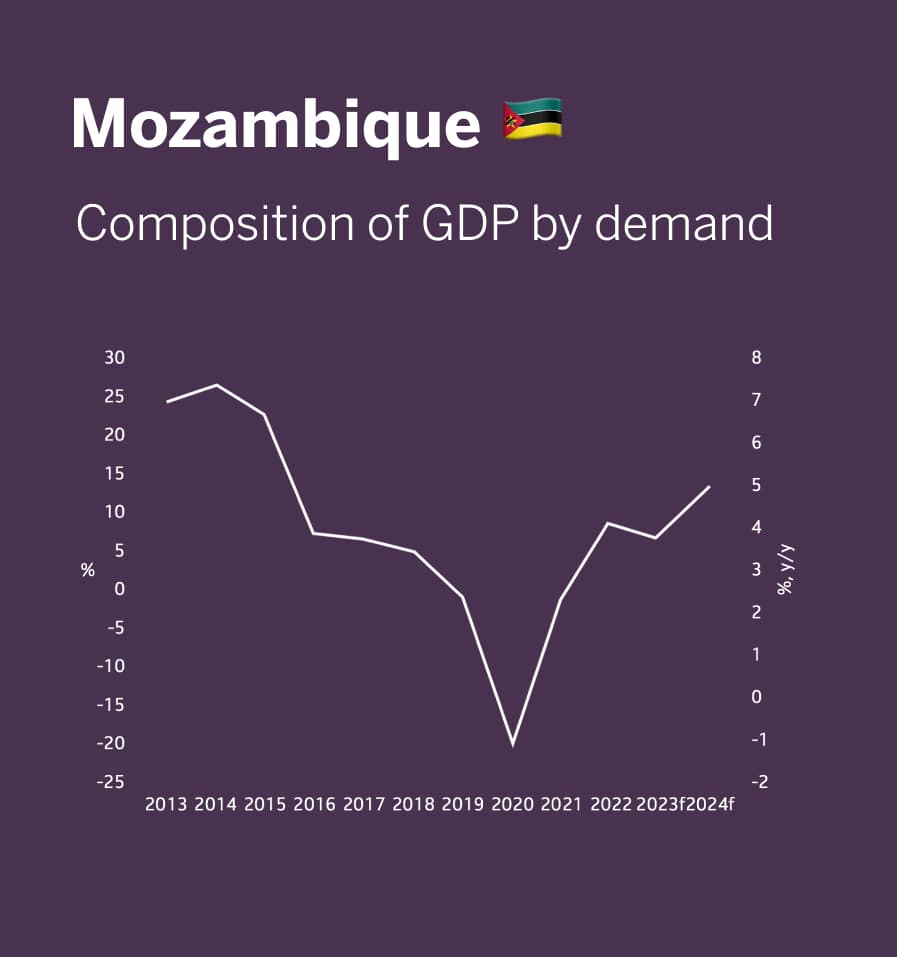

While heavy El Niño rains could be detrimental to East African growth, a more moderate impact on infrastructure might benefit the region by moderating food inflation and bolstering private consumption expenditure. Yet, the historical impact of El Niño may not offer a precise prediction due to advancements in technology and infrastructure. Southern African economies, though likely to experience drier weather during El Niño, may experience a less severe impact on growth compared to their eastern counterparts due to their smaller agricultural sector contributions to GDP. Downside risks, however, loom for Malawi and Mozambique, both grappling with the aftermath of climate change consequences from cyclone Freddy. Additionally, developments in Zambia’s external debt restructuring under the G20 common framework and the potential for debt restructuring in Ghana in H2:23 show progress on the continent. Nevertheless, persistent FX liquidity concerns and expected increases in short-term interest rates in Kenya indicate ongoing challenges in the African economic landscape.

Markets

WHAT TO WATCH NEXT

Africa is our home. And has been for over 160 years. Today our commitment to her people and her prosperity is stronger than ever. Because when this continent wins, economies grow, communities thrive and our clients succeed.

The summit builds on 2022’s Net zero theme, focussing on climate change in the context of energy access and energy transition, while acknowledging the link to ESG.

When women become leaders, they have the capability to make bold decisions that drive meaningful change and transform industries.

The African Central Bank Conference hosts regulators and central bank officials from across the continent. The key themes focus on the broader monetary policy environment, on financial market development, and on strategic responses to shared challenges. The aim of the conference is to raise awareness of the pipeline of innovative solutions across different countries as it is key for African sovereigns to form partnerships with institutional investors as the controllers of the largest pool of assets available for long-term investing.

Mercer, in collaboration with MiDA Advisors and Standard Bank Group have joined forces to publish the second edition of the Mercer report publication titled “Infrastructure financing in sub-Saharan Africa” to present the attractive case for investing in Africa.

When women become leaders, they have the capability to make bold decisions that drive meaningful change and transform industries.

The summit builds on 2021’s Net-Zero theme, focussing on climate change in the context of energy access and energy transition, while acknowledging the link to ESG.

As Standard Bank, we will transform client experience; execute with excellence; and drive sustainable growth.

The 9th annual South Africa Tomorrow Conference, a showcase of African Institutions and listed companies, under the topical theme this year of ‘Structural Reform and Catalysts for Growth’