We forecast growth of 6.9% y/y in 2022 and 6.6% y/y in 2023. We expect the C/A deficit to widen to 3.5% of GDP in 2022. We see the pair USD/XOF around 599 by Dec 22.

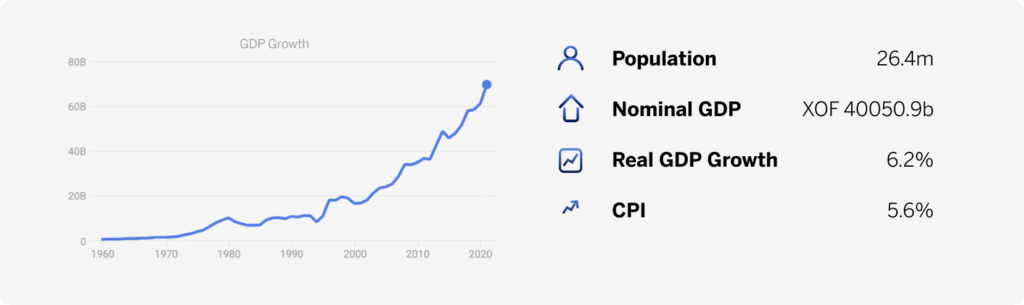

GDP growth

We forecast growth of 6.9%y/y in 2022. The implementation of the new national development plan, alongside growth in agricultural, services and construction sectors will propel growth in 2022. In 2023, tourism and transport, construction sector would benefit from the African cup of Nations.

However, poor capacity in electricity sector poses a downside risk to growth in near term. Although, the use of cocoa waste at the DIVO biomass power plant may boost future electricity production.

While Q3:21 GDP growth of 5%y/y was supported by the tertiary sector and secondary sector, the primary sector contracted as the poor rainfall during the period affected agricultural output.

Balance of payments

We expect C/A to widen to 3.5% of GDP as primary income (rising debt service cost and profit repatriation) may weigh on the current account.

Furthermore, the Ukraine and Russia war pose an upside risk to import as fuel imports are 1.8 times the petroleum products exports. Additionally, the increased investment in the context of NDP 2021-25, to support structural transformation and to boost oil production will further elevate imports. With elevated commodity prices, goods and services exports too should increase.

Monetary policy

While the minimum bid rate and marginal window rate has been steady since mid-2022, we expect the MPC to start tightening policy towards the end of the year.

We see headline inflation reaching 3.5% y/y by Dec from 4.2% in 2021. Supply disruptions and higher global commodity prices could pressure inflation in the region. However, base effect may keep inflation contained in H2:22.

FX outlook

Following longer term costs to the eurozone economy from the Ukraine war, we expect a wider spread btw the US and eurozone implying a weaker euro. Hence, our euro/dollar forecast has been cut back from 1.4. The bias is for USD/XOF to reach a peak of 643 before declining to 599 by Dec.

Download the annual indicators.