DRC: robust extractive sector still supporting resilient growth

Medium-term outlook: extractive sector and structural reforms both growth-supportive

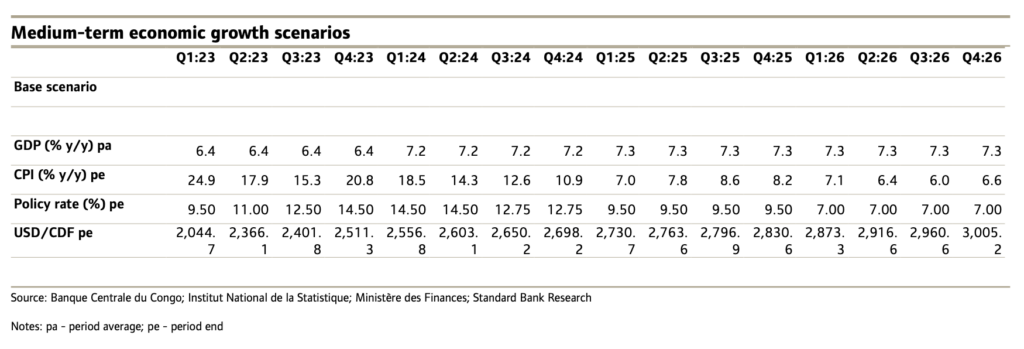

Though we see GDP growth slowing to 6.4% y/y this year due to rising inflation and monetary policy tightening, there should be a recovery in 2024, to 7.2% y/y, as inflation may ease.

Intermittently poor FX liquidity has seen the Congolese franc depreciate, which increases imported inflation. Inflation also still faces the general elections (Dec this year).

Insecurity in DRC has inflated domestic food prices and caused a humanitarian crisis. Inflation being stubbornly high also reflects second round spill-over effects from the war in Ukraine causing global food and fuel prices to increase.

President Tshisekedi, inaugurated in Sep 19, will run for a second term. DRC had recorded its first ever peaceful power transition after the 2018 general elections.

Nevertheless, despite armed conflict in eastern parts of DRC, the economy has proven robust thanks to a strong performance from the resources sector. GDP growth rose to 8.9% y/y in 2022, from 6.2% y/y in 2021, and exceeding by 2.5 percentages points our estimates in the Jan AMR edition. Copper and cobalt output was strong, accounting for 70% and 20% respectively of exports.

Copper output rose by 32.8% y/y in 2022, to 2.4 mtpa, from 1.8 mtpa in 2021, mainly due to the production ramp-up at the Kamoa copper mine complex, set to become the second-largest copper mine in the world. Cobalt grew at 23.9% y/y in 2022, to 115.4 k tons.

Foreign direct investment into the resources sector, which lifts output and supports exports, should continue apace – considering the role of copper, and other DRC minerals, in the global energy transition.

However, despite DRC having vast natural resources, over 77% of the population lives below the poverty line of purchasing power parity (PPP) of USD1.9/day. This is largely due to domestic conflicts.

To deal with climate risks, the government has requested access to the IMF’s Resilience and Stability Facility (RSF); there should be some progress during H2:23.

Progress on reforms, supported by the current IMF 3-y ECF, which also helps to unlock multilateral funding, should alleviate FX liquidity pressures and support growth.

The growth outlook remains positive but is subject to the downside risks embodied by commodity price volatility and domestic insecurity.