Egypt: privatisation pace still too patchy

Medium-term outlook: downside risks to growth

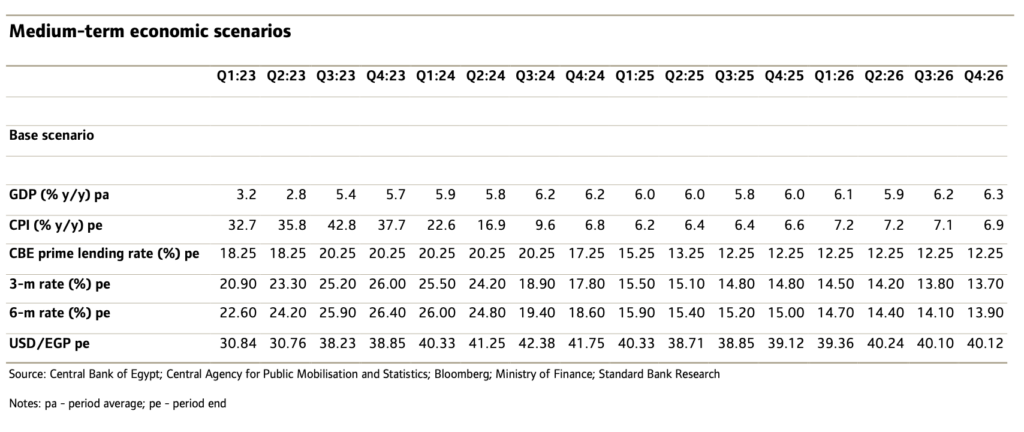

We now reduce our FY2022/23 GDP growth forecast to 4.1% y/y – 4.4% y/y, from 4.8% – 5.2% y/y. Our FY2023/24 growth forecast too is lower, at 4.9% y/y – 5.3% y/y, from 5.7% y/y – 6.0% y/y.

Economic activity subsided in H1:23, per most leading economic indicators – such as the PMI which averaged 46.8 in the 5-m to May 23, from 47.1 in the 5-m to Dec 22.

Growth has been hampered by instability in macroeconomic conditions; mainly, rising inflation and little USD liquidity. This has also hindered both private consumption and investment.

Since the rise in geopolitical tensions in Q1:22, food prices, specifically wheat, are up sharply, adding to the strain of declining private consumption. The Egyptian authorities in response increased wheat prices by 20% for the 2023 harvest season, aiming to incentivise farmers to boost local production. Meantime, however, real income may decline further and thereby weigh on growth.

The further devaluation of the EGP in Q1:23 may have subdued growth across many sectors, with the manufacturing sector bearing the brunt despite the re-opening of the Chinese economy in Q4:22 restoring supply chains.

Growth in the manufacturing sub-sector contracted by 1.8% y/y in Q4:22, from growth of 1.3% y/y and 5.8% y/y in Q3:22 and Q2:22 respectively.

A further devaluation in the EGP is already being priced in by the market; this would undoubtedly increase manufacturing input costs. Amidst weaker domestic demand, passing on higher input costs as output costs to consumers would be tricky.

Even without further EGP devaluation, poor FX liquidity may still subdue growth for many sectors.

Furthermore, relatively lower oil prices, and Egypt’s constrained macroeconomy, may subdue investment in the mining and petroleum sectors over the coming year.