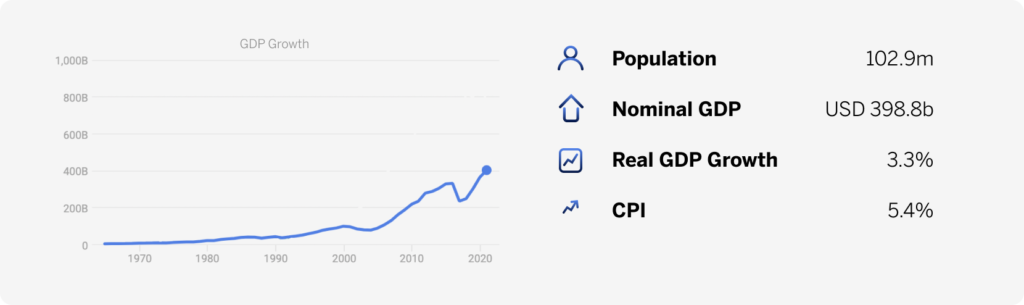

We expect GDP to grow by 5.4% y/y in 2022 before improving to 4.8% y/y in 2023. The C/A deficit will likely widen to 7.3% of GDP in 2022 before narrowing to 5.1% of GDP in 2023. We expect USD/EGP pair to close the year around 18.50.

Medium-term outlook- relatively resilient, but still with downside risks

Despite notable economic headwinds in H1:22, we now raise our GDP growth forecast to 5.2% y/y-5.5% y/y for FY2021/22, from 4.8% y/y-5.2% y/y, due to likely stronger-thanexpected growth in H2:21. However, we lower our FY2022/23 growth forecast to 4.7% y/y5.0% y/y, from 5.3% y/y-5.6% y/y. Of the markets in our coverage, Egypt is perhaps the most exposed to the Ukraine war. Unfavourable base effects too may restrain GDP growth in H2:22, while the second-round impacts of higher fuel and food prices may keep aggregate demand subdued. In addition, the recent devaluation of the EGP may dampen consumer spending over the next 6-m. Furthermore, with the Central Bank of Egypt’s MPC likely to tighten monetary policy further amidst rising underlying inflation pressure, private investment may decline, also weighing on growth. The government’s public infrastructure investment too should support growth in 2023. However, with an IMF funded program imminent, the government may have to scale back on development expenditure to ensure that public debt remains sustainable.

Balance of payments – C/A deficit to deepen

We now expect the C/A deficit to deepen to 7.3% of GDP in 2022, from our prior forecast of 5.9% of GDP. Thereafter, in 2023, it should narrow to 5.1% of GDP. The government’s import requirement for food is likely to increase notably over the coming year due to its reliance on wheat imports from Russia and Ukraine.

Furthermore, the sharp rise in international oil prices will swell the oil import bill. Egypt’s reliance on Russia and Ukraine as tourism source markets may also weigh down the services balance. Moreover, the global risk-off sentiment brought about the Ukraine war, and tighter monetary policy in advanced economies, have already exacerbated BOP pressures in Egypt. Foreign portfolio investors have been selling off their holdings in EGP local debt, while the rise in Egypt’s Eurobond yields has made it difficult for the government to issue new Eurobonds. However, an IMF-funded program is imminent. We expect this funding to be worth between USD10.0-12.0bn and likely to be secured before end Q3:22. This funding which could be spread out over three years at least, will hugely assist in financing the wider C/A deficit over the next few years.

Monetary policy- tightening bias

We expect the MPC to increase the key benchmark rate by a further 150-250 bps this year. While headline inflation was expected to rise after the EGP devaluation and spiking of food and fuel prices, it has done so much faster than we had anticipated. The MPC will probably continue to raise rates to tame spiralling inflation expectations. Indeed, the upcoming IMF program may require the authorities to now adopt a more restrictive monetary policy stance to curb inflationary risks. We now expect headline inflation to rise to 16.4% y/y in Jun and 16.7% y/y in Sep 22, then ease to 15.0% y/y in Dec 22. Headline inflation may even slide below the government’s 9.0% upper band target in May 23, and average 5.8% y/y in H2:23. If so, the MPC may become more accommodative in H2:23 as inflationary pressures ease. That however would be largely contingent on the second-round effects of higher oil prices as well as a weaker EGP not becoming entrenched.

FX outlook – USD/EGP upward bias

We see the USD/EGP pair at 18.50-18.70 by end 2022. The EGP was devalued by c.14% in Mar 21; the market since has seemed unsure about the EGP’s trajectory. Still, most of this recent EGP overvaluation has likely been addressed; we therefore foresee little pressure by the authorities to abruptly weaken the local unit by a similar magnitude as the recent

devaluation.

However, given the broad view that the EGP was pegged over the last 3-y, it remains unclear whether this upward adjustment may simply become a new tight range for the peg, or whether the EGP may freely float. Still, with an IMF funded program imminent, the Fund would likely want the EGP to act more as shock absorber as well as show some flexibility. Given a likely wider C/A deficit and patchy global sentiment, EGP may be slightly weaker by Dec.

Download the annual indicators.