Ethiopia: a telecom and mobile money licence windfall

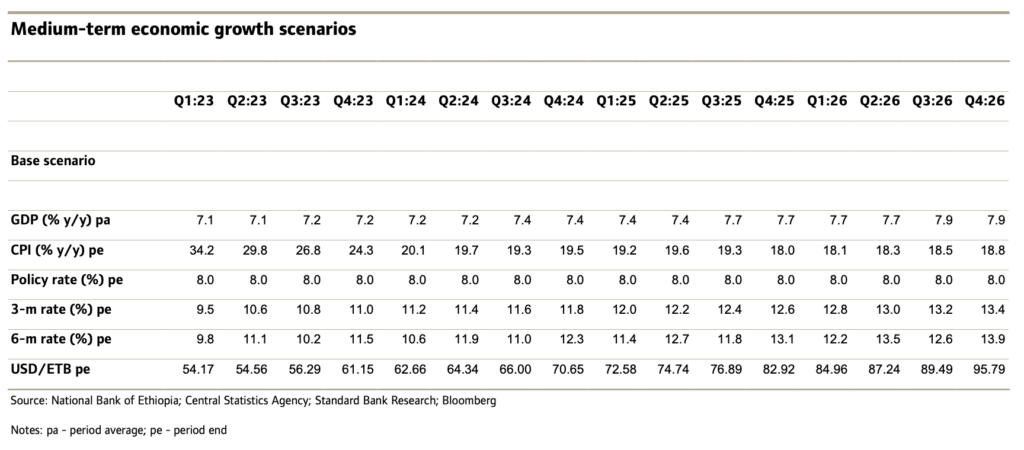

We maintain our GDP growth forecasts of 7.1% y/y for FY2023 and 7.2% y/y for FY2024. Prolonged debt restructuring may constrain medium-term GDP growth. However, ongoing reforms, and the windfall from telecom and mobile money licences, should boost growth. Indeed, IFC and MIGA recently announced a USD157.4m equity investment, a USD100m loan, and a USD1.0bn 10-year guarantee to support the ongoing construction and operation of Safaricom Ethiopia’s greenfield telecommunications network.

Besides the revenue generated by way of licence fees, other permanent benefits from telecom privatisation, such as new technology, innovation and competition for telecommunications providers, should mean competitive prices for businesses and consumers. Moreover, this should also mean longer-term commitments, as well as new skills, and job creation.

GDP growth in FY2022 was 6.4% y/y, exceeding market estimates considerably. This gain was ascribed to 7.6% y/y growth in the services sector, 6.1% y/y growth in agriculture, and 4.9% y/y growth in industry. As a result, the share of GDP accounted for by services increased to 40%, from 39.6% a year ago.

Despite several uncertainties, including the usual potential drought, the government’s focus on growing industrial output is expected to remain the cornerstone of its medium-term economic strategy. Drought is a possibility given the El Niño event predicted as of H2:23. Although this weather pattern bodes well for East African rainfall, it can cause extensive drought in the eastern, southern and central parts of Ethiopia. In fact, during the 2015-16 El Niño episode, crop failure and food insecurity were caused by failing Belg and delayed/erratic Kiremt. However, by the time of this year’s expected El Niño, the main planting seasons in Belg (Feb to May) and Kiremt (Jun to Sept) should have been completed.

Despite a 16.8% y/y cut in the capital budget, public infrastructure investment may further promote GDP growth in the coming years. Although infrastructure-led growth has lost momentum, things may be different now that the government is focusing its resources on completing projects near completion and that are therefore likely to boost productivity.

Still, a significant constraint to medium-term economic growth is persistently poor FX liquidity.

The government will likely continue with economic reforms to make GDP growth more inclusive, with the private sector likely becoming a more dominant driver of growth.