We lower GDP growth to 3.1% y/y in 2022 and 4.1% y/y in 2023. We expect the C/A deficit to widen to 4.1% of GDP in 2022, then narrow to 2.6% in 2023. We expect USD/GHS to rise to 8.29 by year-end.

GDP growth – emerging risks

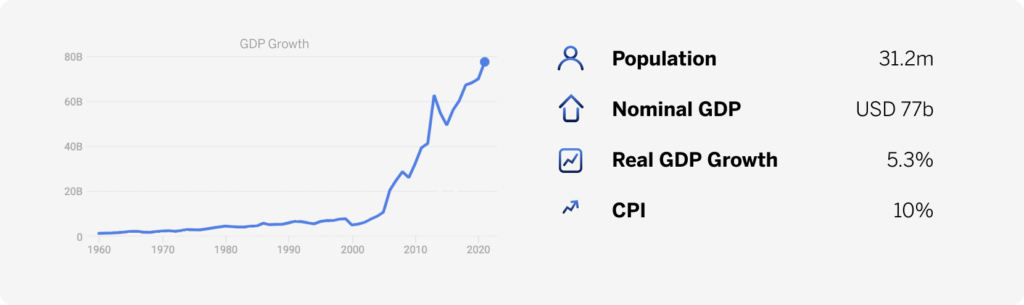

We slash our GDP growth forecast to 3.1% y/y for 2022, from 6.2% y/y. We also lower our 2023 growth forecast to 4.1% y/y, from 6.8% y/y in our Jan AMR publication. GDP growth recovered to 5.3% y/y in 2021; however, growth now faces a confluence of downside risks this year and next. Firstly, the government is running out of external financing options; therefore, public investment in infrastructure is unlikely to underpin growth over the coming year. Secondly, the GHS’s plummet since Jan has further bumped up inflation, which would soften private household consumption over the coming year. Therefore, the BOG’s MPC may have to further raise the key benchmark rate to stem rising inflation expectations as well as support the GHS. This may also further reduce private investment over the coming year. GDP growth also faces rising domestic fuel prices, and with no fuel subsidies to offer any support. Still, the gold sector may offer some upside to our outlook. Off its low base of 2021, gold production should therefore recover, based on key mines’ forecasts.

Balance of payments – no external funding

We now expect the C/A deficit to widen to 4.1% of GDP in 2022, then narrow to 2.6% in 2023. Still, financing a wider C/A deficit in 2022 would prove near impossible due to the lack of external funding. Authorities have publicly ruled out seeking another IMF-funded program. Also, the steep increase in Ghana’s Eurobond yields effectively shuts the door to any such commercial financing.

Cocoa exports too may soften this year due to fertilizer price hikes –but gold exports should recover from a low base. But even gold exports face downward pressure, with the USD index now broadly stronger which could dampen international gold prices. Imports could increase owing to more expensive input prices such as those of fertilizer. However, as the MPC continues to potentially tighten its policy stance further, consumer import demand could ease.

Monetary policy – further tightening

We expect the MPC to hike its key policy rate by a further 100-150 bps in 2022. Inflationary pressures are accelerating; the MPC clearly stated its intention to tame that by its aggressive 450 bps hike of the policy rate, to 19.0%, between Mar and May. After the GHS found some stability following that hike, this may see the MPC standing pat. However, the lack of external funding may deplete FX reserves as well as the MPC’s ability to mitigate USD/GHS volatility. Inflationary pressures may become more entrenched, should the government fail to secure IMF funding, international oil prices remain elevated, and global risk appetite worsens further.

FX outlook – GHS may weaken further

We expect USD/GHS to rise to 8.29 by Dec. The GHS has been under immense pressure since Jan due to further foreign portfolio outflows. However, after the Mar rate hike, the pair had stabilised around 7.50. Still, monetary policy can perhaps only do so much to stabilise the GHS; its selloff has been driven mainly by the concerns around fiscal policy. Should the government secure an IMF deal in 2023, the GHS would benefit enormously. But, in the meantime, it will weaken, especially as global risk worsens further.

Download the annual indicators.