Mozambique: LNG to support growth

Medium-term outlook: hefty LNG investments

It may be 4-5y before liquified natural gas (LNG) investments can make a meaningful contribution to Mozambique’s fiscus, depending on the quantum of LNG output and income. Still, as investments increase, GDP growth too should speed up.

Planned investment for the next 3 LNG projects (the resumption of TotalEnergies LNG in H2:23, final investment decisions for ExxonMobil and ENI’s 2nd FLNG projects in 2024), estimated at USD55bn, or nearly 3x 2022 GDP (USD19.2bn), spell an LNG boom as of 2027, foretelling fiscal support.

Mozambique still faces subdued GDP growth (besides the resources sector), and lower fiscal revenue, which has aggravated fiscal risks and pressures – exacerbated by the high wage bill and therefore sharply higher domestic debt.

The external position too is fragile due to large current account deficits (besides large projects), cyclical climate shocks, and frequent terms-of-trade shocks.

All this has seen the Banco de Moçambique further tightening monetary policy in H1:23 by transferring from commercial banks over 12% of GDP in cash required reserves – to address increased risks, while helping to lower inflation (which slid to 8.2% y/y in May after dwelling in double digits for most of the past 12-m).

Tighter financing and liquidity conditions will likely subdue personal consumption expenditure (PCE) and government expenditure (GE), even with municipal elections due next Oct.

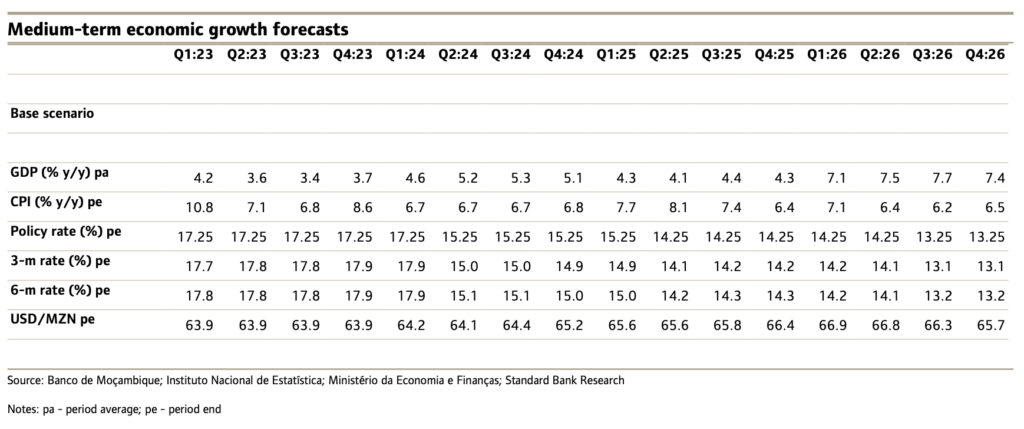

Our GDP growth forecasts for 2023 now slightly undershoot those we had in the Jan AMR edition. We now see growth decelerating to 3.7% y/y this year, from 4.2% y/y before, due to tighter financing conditions usually subduing growth (besides the extractive sector).

Investment, mostly LNG-related, alongside potential monetary policy easing next year as inflation declines further, and the likely rise in fiscal expenditure ahead of the Oct 24 general elections, may see growth at 5.1% y/y in 2024.

Per Instituto Nacional de Estatística (INE) data, GDP grew 4.2% y/y in Q1:23, matching that of Q4:22 as well as all of 2022. Q1:23 growth underpins a 32.6% y/y rise in extractive sector output, an acceleration from 13.2% y/y in Q4:22, due to the production ramp-up at ENI’s Coral South FLNG plant, with 3.4 mtpa nominal capacity; exports began in Nov 22. Besides extractives, growth decelerated to 2.7% y/y in Q1:23, from 3.5% y/y in Q4:22, due to manufacturing and construction remaining in recession and adverse weather impelling softer growth in agriculture, of 3.8% y/y, down from 6.2% y/y.