Namibia: buoyed by mining and green hydrogen prospects

Medium-term outlook: mining sector upside

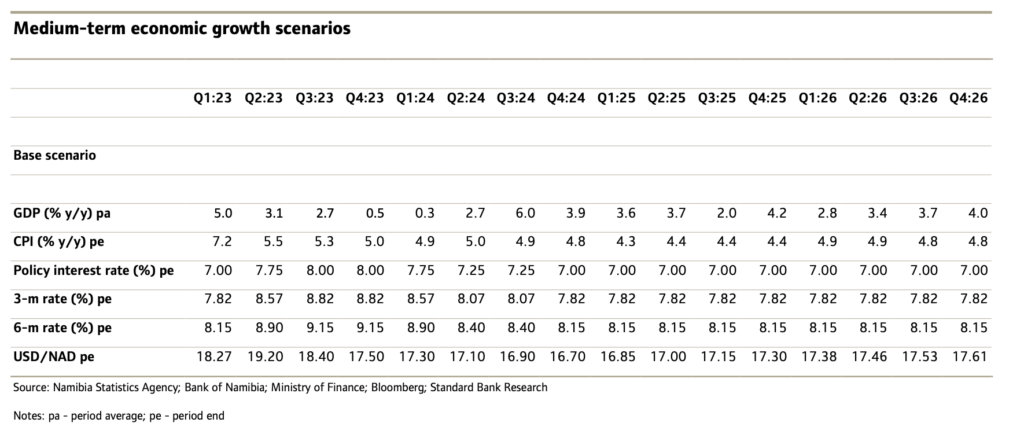

We retain our 2023 GDP growth forecast at 2.8% y/y. In 2022, growth was a robust 4.6% y/y. However, we now trim our 2024 growth forecast to 3.2% y/y, from 3.5% y/y. As of 2025-2026, we would foresee average growth of 3.4%.

We had forecast Q1:23 at 2.6% y/y – but growth expanded by 5.0% y/y, from 2.1% y/y in Q4:22. This however still undershot 7.3% y/growth for Q1:22. Slower growth in Q1:23 was mainly due to declines in the financial services and manufacturing sectors, respectively contracting by 4.9% y/y and 2.7% y/y.

Mining and quarrying however posted a stellar performance of 34.3% y/y and 18% q/q respectively, contributing 3.7 percentage points to GDP growth. There was further mineral exploration activity as well as investment in mining. Indeed, this sector should underpin growth in 2023; it had posted growth of 21.6% y/y in 2022. Besides exploration activities, the uranium and diamond sub-sectors too have been growing meaningfully. For the first 4-m of this year, uranium production was up 27.3% y/y over the 4.1% y/y contraction over the same period last year. With the global policy shift to support nuclear power as a cleaner and more sustainable energy source, we are optimistic about uranium demand and production. Diamond production too was higher during Jan-Apr, at 805.9k carats, from 624.k carats over the same period in 2022. With the global outlook for 2023 revised lower by the IMF, demand could falter.

With the government now having signed a partnership agreement with the developer for the next phase of the USD10bn green hydrogen project, this too should support growth. Namibia intends to ship its first green hydrogen exports by 2026 (a 125,000 tonne first phase).

No final investment decision (FID) has been announced yet for the two recent offshore oil discoveries; still, both should prove to boost both this economy, as well as per-capita GDP, tremendously in the long term.

The tourism sector too has been recovering meaningfully, though it remains below the pre-pandemic level of 1.6m tourists a year. Tourist arrivals, a proxy for activity in this sector, hit 331, 560 in 2022 (2021 arrivals were 232,756).

That said, with higher probabilities of an El Niño this year, this may harm the already fragile agriculture sector. In Q1:23, it grew moderately, by 3.6% y/y, from the 8.1% y/y in Q1:22, but still down 59% q/q due to inadequate rainfall constraining the crop farming subsector.

Further downside risks to our growth outlook include domestic and global monetary tightening undermining demand. An economic slowdown in Europe, a major tourist partner, too may limit tourism.