We expect GDP growth of 3.2% y/y in 2022 and 3.3% y/y in 2023. We expect a C/A surplus of 2% of GDP in 2022 and 1.5% of GDP in 2023. We see the pair USD/NGN around 440 at year-end.

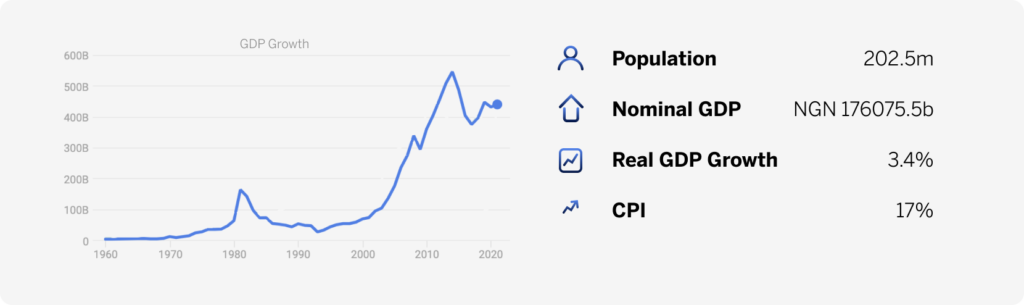

GDP growth

Nigeria’s GDP growth may reach 3.2% y/y in 2022 and 3.3% y/y in 2023. Growth drivers in the last few quarters were agriculture, trade, ICT, manufacturing, and construction, which may recur this year. The oil sector promises little or no improvement near term; it has been in contraction for 7-q already. Oil theft and pipeline vandalism remain bugbears. Additionally, precarious power supply and insecurity in the food belt poses a downside risk.

Balance of payments

We forecast a current account surplus of 2.0% of GDP by end 2022 and 1.5% of GDP by end 2023 as high oil prices should support the trade balance. Supply-chain constraints may further exacerbate trade disruptions, with a knock-on effect for ongoing projects. The Dangote fertilizer plant, set to open in Q3:22, may therefore face delays.

The services account will remain in deficit. In the first 3-q of 2021, the deficit was narrower given CBN’s FX demand management stance. Furthermore, banks have been imposing stricter restrictions on international payments to manage FX demand. External debt will likely finance the BOP as FDI and FPI flows may both lag during the period.

Monetary policy

The MPC at it May meeting hiked the MPR to 13% to contain inflationary pressures and following the monetary policy tightening spree seen globally. We expect inflation to remain sticky, averaging 16.8% this year. However, should inflation keep rising, the MPC might intervene again to contain inflation expectations. Further upside risk is posed by rising energy prices affecting price of deregulated petroleum products such as diesel, kerosene and jet fuel, as well as further supply-chain disruptions globally. For now, however, the petrol subsidy should help to contain inflation.

FX outlook

We forecast the USD/NGN pair at 440 by Dec; Despite ample FX reserves, the CBN has maintained gradual FX intervention for FPIs and corporates. The current demand backlog is likely USD 800m-USD1bn, and the corporate backlog USD2.5bn. The CBN has introduced a RT200 FX policy to improve FX repatriation from non-oil exports to USD200bn in the next 3 to 5-y. In the long term, this may buffer FX liquidity.

Download the annual indicators.