GDP growth is forecast at 7.4% y/y in 2022 and 7.3% y/y in 2023. We still forecast the C/A deficit to widen to 13.2% of GDP in 2022 and 12.0% in 2023. We expect USD/RWF trading at 1051.6 by end 2022.

Medium-term outlook: recovery well underway

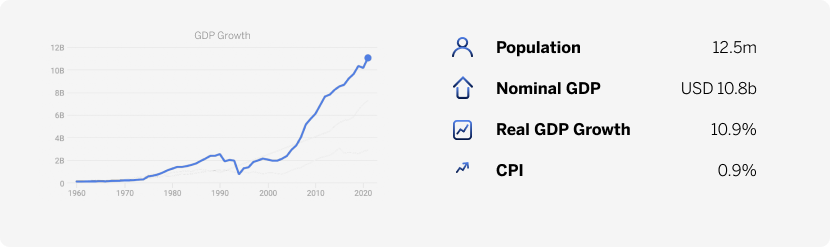

We see GDP growth in Rwanda reaching 7.4% y/y in 2022, from 10.9% y/y in 2021. The postpandemic economic recovery is well underway; however, unfavourable base effects will likely limit GDP growth in 2022. Furthermore, rising inflation may constrain private sector consumption. Public health restrictions will likely be neither as severe nor as disruptive as during 2020. Indeed, we foresee minimal public health restrictions as the focus has now shifted to vaccination. Though the agricultural sector contributes to 24% to GDP, it contributes more significantly to formal employment, with a large part of the population relying on subsistence agriculture. A strong agricultural outturn would still bode well for overall economic prosperity.

However, as fertilizer prices earlier this year rose sharply due to the Ukraine war, Rwanda’s Agriculture Ministry is rationing farmers’ supplies of fertilizer. Moreover, some farmers have delayed planting as a result. This may weigh on agricultural output during the upcoming harvest season despite favourable rainfall.

Balance of Payment – fuel and fertilizer prices inflate imports

The C/A deficit will likely stay wide at 13.2% of GDP in 2022 and 12% of GDP in 2023. At end 2021, the C/A deficit was 10.3% of GDP (or USD1.2bn). Higher fuel and fertilizer prices will most likely inflate the import bill. The Russia-Ukraine conflict may further disrupt fertilizer supplies to Rwanda; it relies on Russia for around 20% of total fertilizer imports. Moreover, fertilizer rationing will trim crop yields, thereby cutting production. Rwanda’s cash crops, coffee and tea, account for over half of traditional goods export earnings, thereby exposing the export base to both climate change risks as well as adverse weather.

However, as the economic recovery continues, consumer and intermediary goods imports should pick up. Due to some public health restrictions persisting, the recovery in tourism receipts may still lag in 2022, then recover more robustly in 2023. Rwanda’s capital and financial accounts are dominated by external government borrowing and direct investment. Rwanda has revised the Investment Code, introduced new priority sectors and activities and announced new tax incentives for certain investor groupings, which should encourage a further rise in FDI inflows.

Monetary policy – inflationary risks

The National Bank of Rwanda (NBR) saw inflation testing its upper band of 8% its target range in 2022, which motivated the MPC to increase the policy rate by 50 bps at the Feb meeting. The policy rate is now 5%. However, we expect the MPC to hold the policy rate unchanged for the remainder of the year while it accesses the impact of the Feb rate hike. Still, should inflation surprise to the upside, the MPC may hike again. We see annual urban inflation averaging 8.9% in 2022 and 4.5% in 2023. Furthermore, higher fuel and fertilizer prices may push both food and non-food inflation up further.

FX outlook – moderate, gradual, depreciation

We see the USD/RWF at around 1,052 at end 2022 and 1,103 at end 2023. Gradual currency depreciation will likely continue in 2022. Indeed, the RWF depreciated by 3.89% against the USD in 2021 and 5.05% in 2020. Foreign aid inflows have remained strong, a key factor supporting the RWF. This should continue in 2022. However, with imports rising, a likely higher import bill may underpin onshore FX liquidity challenges. Our bear case models elevated external pressures.

We forecast a higher rate of depreciation, putting the USD/RWF at 1,155 by mid-2023. Credit to the private sector reached to 14.7% y/y at end 2021, from 21.8% y/y at end 2020, largely driven by an increase in new loans. Credit

extension to the private sector was inflated by the restructuring of loans for reasons of pandemic-related distress. Furthermore, a tighter policy stance may limit new credit extension.

Download the annual indicators.