Senegal: hydrocarbon production should spur growth

Medium-term outlook: promising

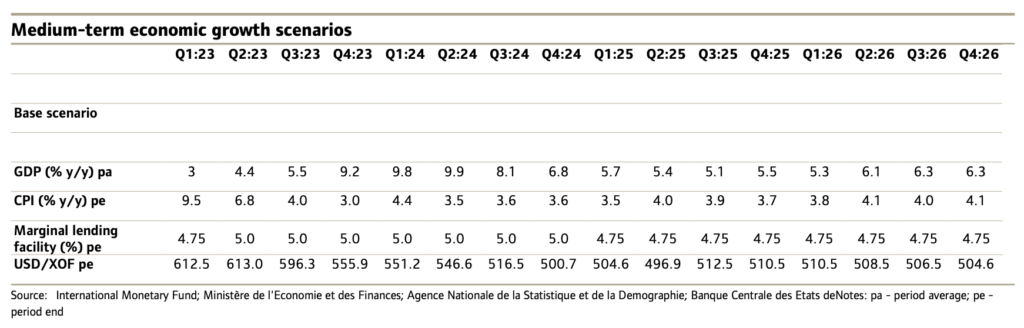

We now forecast real GDP growth at 5.5% for 2023 and then 8.7% in 2024, likely driven by significantly higher exports growth, as well as higher industry growth.

Medium-term economic prospects remain strong, supported by infrastructure projects and the likely commencement of oil and gas production this year. However, growth faces further potential domestic insecurity linked to the upcoming 2024 general elections.

While President Macky Sall claims legal right to run for a third term, he has made no definitive announcement yet. Should he run, we may see another round of violent protests when he confirms his candidacy.

Additionally, Ousmane Sonko, a major opposition potential candidate, was sentenced to 2-y in prison for ‘corrupting the youth’, likely lessening his chances to participate in this election. His sentencing led to violent protests, deaths, and affected economic activity.

In 2022, economic growth slowed, with GDP growth decreasing to 4% y/y, from 6.5% y/y in 2021. Food and energy prices had soared due to the Ukraine invasion, harvests were poor, and industrial production low. Real export growth declined to 8.1% in 2022, from 22.6% in 2021, mainly due to reduced external demand and the temporary closure of borders.

This year, economic activity should rebound. The outlook though will rely largely on hydrocarbon production prospects. Hydrocarbon production is likely to begin by Q4:23, playing fully out as of 2024.

The medium-term outlook is still positive due to the commencement of oil and gas production and the implementation of structural reforms aimed at enhancing private-sector participation.

However, there are downside risks by way of potential delays in hydrocarbon production, election-related expenses, and entrenched energy subsidies.