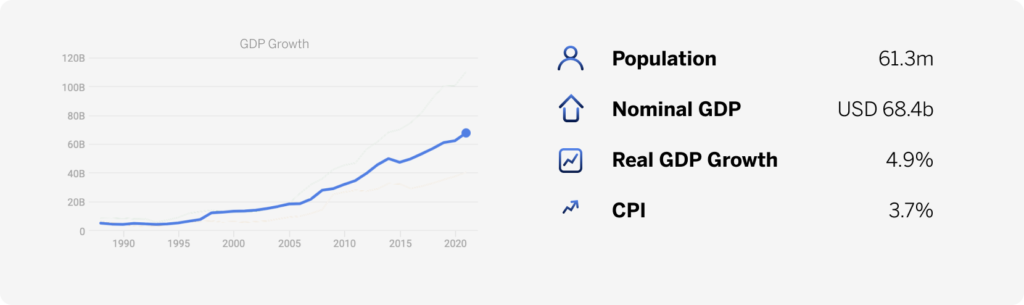

We expect GDP growth to expand by 6.0% y/y in 2022 and 6.3% in 2023. We see the C/A deficit widening to 4.7% of GDP in 2022 and narrowing to 4.1% of GDP in 2023. We see USD/TZS trading close to 2322 by the end of 2022.

Medium-term outlook: fewer productivity gains from infrastructure spending

We now trim our 2022 GDP growth forecast to 6.0% y/y, from 6.4% y/y, due to geopolitical factors and fewer productivity gains from infrastructure spending. We also cut our forecast for 2023 to 6.3% y/y, from 7.3% y/y, foreseeing this economy slowing further in 2023. Despite so many destructive geopolitical events in H1:22, growth may benefit numerically from favourable base effects. In H1:21, a further wave of Covid, coupled with a regime change, slowed down growth.

The Ukraine war has sharply bumped up energy and fertilizer prices, and China’s renewed widespread lockdowns have exacerbated in supply-chain troubles, thereby inflating freight costs. Higher fertilizer prices might crimp agricultural output in 2022, with higher energy and freight costs swelling companies’ input costs as well as inflation. Should both become entrenched, growth, particularly in H2:22, may slow down. The government should be increasingly supporting positive private sector reforms because productivity gains from public infrastructure projects are waning. Growth in the construction and transport sectors, the main beneficiaries of the projects, is slowing.

Balance of payments – widening C/A deficit

We expect the C/A deficit to widen from 3.0% of GDP in 2021 to 4.7% in 2022, then narrow to 4.1% in 2023. Such a larger C/A deficit would be due to a worsening trade deficit because of geopolitical factors. The China lockdowns and Ukraine war may well incur a larger trade deficit as import prices rocket and export volumes slide. Service receipts, however, could recover further, based on the reduction in public health restrictions globally. The larger C/A deficit is likely to be financed by external debt receipts. Rising USD interest rates could make it expensive for the government to tap external commercial debt markets through syndicated loans. The government has announced plans to seek concessionary debt from the IMF (of about USD700m) and the World Bank.

Monetary policy – neutral in 2022

The MPC will likely keep the policy rate unchanged at 5.0% this year to support private sector credit growth and, consequently, growth in aggregate demand. Inflation may remain within BOT (Bank of Tanzania) targets in 2022, and the TZS may weaken gradually. However, should inflation rise significantly, and the TZS weaken rapidly due to geopolitical risks, tighter monetary policy may result via a significant rate hike. We see a partial recovery in private sector credit growth in H1:22 driven by credit demand as well as by improved credit supply after banking sector reforms that incentivize lending at lower rates. We see inflation remaining broadly within target.

We forecast inflation to average 3.9% in 2022, from 3.7% in 2021, due to rising energy and food inflation. The increase in energy inflation might be moderated by TZS100bn in fuel subsidies as of Jun. Any significant adjustment in the exchange rate might further bump up inflation and thereby encourage the MPC to act. However, even if the policy rate were hiked, the inadequate transmission mechanism may mean that a hike is a mere signalling tool. The government would then have to resort to either repos or further reforms to moderate excess liquidity sustainably.

FX outlook – weaker TZS and FX liquidity issues

We expect the USD/TZS to weaken this year, ending Dec at 2321-2333, due to a deeper trade deficit, dividend repatriations, and external debt repayments. FX illiquidity too may persist. The TZS tends be relatively stable, with occasional sharp adjustments. The reports of FX illiquidity are now more pronounced than in previous years. There might even be a similarly sharp depreciation in 2022 to attract USD from exporters and alleviate liquidity problems. Due to upcoming debt repayments, the Bank of Tanzania is unlikely to intervene by selling a significant amount of USD. In fact, over the past 5-m, FX reserves have been sliding by an average of USD200m per month due to such debt repayments.

Download the annual indicators.