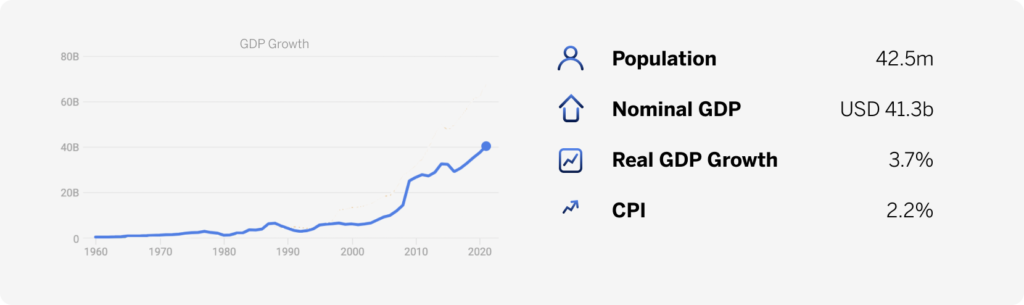

We expect GDP growth of 4.0% y/y in 2022 and 5.7% y/y in 2023. We see the C/A deficit widening to 10.1% of GDP in 2022 and 10.8% of GDP in 2023. We place USD/UGX at 3680-3730 by end 2022.

GDP growth – still robust, should expected oil investment transpire

We now forecast FY2021/22 growth of 4.0%-4.3% y/y, from 4.5%-4.8% y/y previously. We also trim our FY2022/23 forecast to 5.5%-5.8% y/y, from 6.0%-6.3% y/y. The full re-opening of the economy as of Jan 22 should have underpinned economic activity; however, the Ukraine war has raised domestical fuel and food prices, which will likely drag down disposable income and reduce private consumption expenditure over the coming year. China’s Covid-19 resurgence might also further delay supplier delivery times and hinder Uganda’s manufacturing sector. Furthermore, Kenya’s political disruptions in Q3:22 might negatively affect the industrial sector as most manufacturers rely on transport routes via the Malaba border in western Kenya. Moreover, owing to growing ESG concerns surrounding the construction of the East Africa Crude Oil Pipeline (EACOP), funding delays seem likely. Nonetheless, we still expect a notable increase in investment spending from the oil sector to support growth over the medium term, particularly with the government focusing on local content policies to ensure inclusive growth.

Balance of payments – gold exports hopeful

We now expect the C/A deficit to widen to 10.1% of GDP in 2022, from 9.9% forecast previously. The steep rise in international oil prices may also widen the trade balance more than we had expected. However, as private consumer imports might lag due to shrinking disposable income, goods imports growth may be more measured than otherwise would have been the case. Over the coming year, tourism and gold receipts may recover. Gold exports were suspended in Jul 21 after the government imposed a flat tax of 5% and 10% respectively on refined and unrefined gold exports. Now, the government has proposed a tax of USD100 for every kilogram of gold exported, pending parliamentary approval. This might appease operators in the mining sector, which could see gold exports recover.

Monetary policy – tightening bias

We expect the MPC to increase the CBR by 50-100 bps over the rest of 2022 to tame rising inflation expectations. Besides higher international oil prices, domestic food prices too have been rising. We see headline inflation easing between Jun and Jul due to seasonal food price declines. However, thereafter, headline inflation could rise to 6.0% y/y in Oct 22 and 6.3% y/y in Jan 23, due predominantly to second-round effects from oil prices. Were USD/UGX to face more intense upward pressure than currently priced into our base case, the MPC may be more cautious on inflation expectations, likely hiking the CBR more aggressively in H2:22.

FX outlook – near-term upside pressure

We see USD/UGX at 3680-3730 by end 2022. We still expect the pair to approach 3700- 3750 in the near term as global financing conditions continue to tighten, thereby bumping up portfolio outflows from the UGX fixed income market. The BOU intervened aggressively by selling FX to commercial banks in Q1:22 to mitigate USD/UGX volatility. This strategy seems likely to continue over the coming year, thereby likely limiting any material USD/UGX upside.

Download the annual indicators.