Zambia: the tide has finally turned

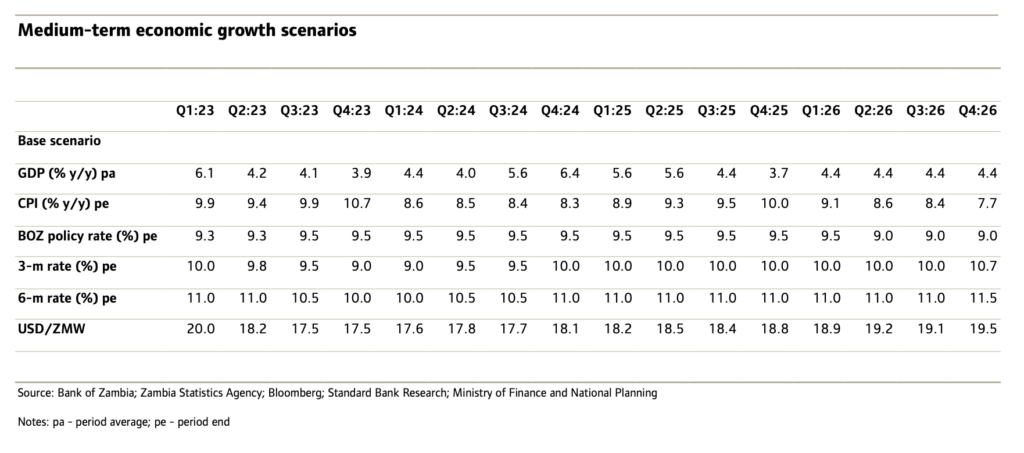

Growth outlook: consumer demand upside and debt restructuring justify optimism

The Government of the Republic of Zambia finally agreed on the terms of their external debt restructuring with official creditors in late Jun 23. USD6.3bn of outstanding debt will be termed out to at least 20-y with a 3-y moratorium on principal payments. Private sector creditors are expected to follow suit. Importantly, investors in local currency bonds are excluded from any treatment, unlike Ghana. Zambia will now be able to access the next tranche of IMF funding of USD188m.

We forecast GDP growth of 4.5% y/y and 5.1% y/y for 2023 and 2024 respectively. GDP grew by 5.8% y/y in Q4:22, bringing 2022 growth to 4.2% y/y. Q4:22 growth was driven mainly by the education, transport and storage, and ICT sub- sectors. However, mining and quarrying remained a drag.

Q1:23 was challenging. Delayed rains meant lower dam water levels, causing electricity generation to plummet by 19% m/m, with a subsequent spike in electricity imports in Jan 23. Delayed rains also drove fears of a weak maize crop, which sent grain prices higher by 41% y/y in Mar 23, which will likely weigh down private consumption expenditure.

Copper export earnings declined as output was lower by 19% y/y in Q1:23, which created negative fundamentals for the kwacha as USD revenue declined. The kwacha also suffered negative sentiment due to little progress on debt restructuring during this period. Copper output thus far in 2023 has been subdued. Total production in Q1: 23 was 143,640 MT, down 19% y/y. This is unlikely to turn around until the KCM and Mopani copper mining firms overhangs have been resolved, which, for Mopani may happen as early as Q3:23.

We nevertheless expect the non-mining sector to star in the growth outlook for 2023. Rains were late but sufficient to replenish water levels and transform the situation from net importing of electricity to net exporting. In addition, officials estimate an 18% y/y increase in maize output, to 3.2 million tonnes, for Q2:23 (although this number is being disputed by observers). However, should the current El Niño weather patterns continue for some years after 2023, hydro-electric power generation and agricultural productivity would be negatively affected. Still, government initiatives should stimulate consumer spending in 2023, benefiting economic growth. For instance, early and partial pension withdrawals, amounting to 2.3% of the 2022 nominal GDP, should boost consumption expenditure. Another initiative is the increase in the allocation and delivery through devolution of the Constituency Development Fund (CDF), projected to constitute 0.9% of 2022 nominal GDP. These measures form part of the government’s strategy to promote economic growth, with results likely in the near to medium-term.